At a Glance

- Global plastic filler market projected to reach $111.4 billion by 2035.

- Packaging, construction, and automotive sectors drive significant demand.

- Calcium carbonate remains the dominant filler type due to its versatility.

The global plastic filler market, valued at USD 62.7 billion in 2023, is poised for substantial growth, with projections indicating it will exceed USD 111.4 billion by 2035, according to a recent report by Market.us. This expansion represents a compound annual growth rate (CAGR) of 4.8% from 2024 to 2035, driven by increasing demand across key industrial sectors. The market's upward trajectory is largely attributed to the growing need for cost-effective and performance-enhancing materials in plastic production. This outlook highlights the enduring and critical role of fillers in modern manufacturing, enabling diverse applications across various industries.

Market Dynamics and Growth Catalysts

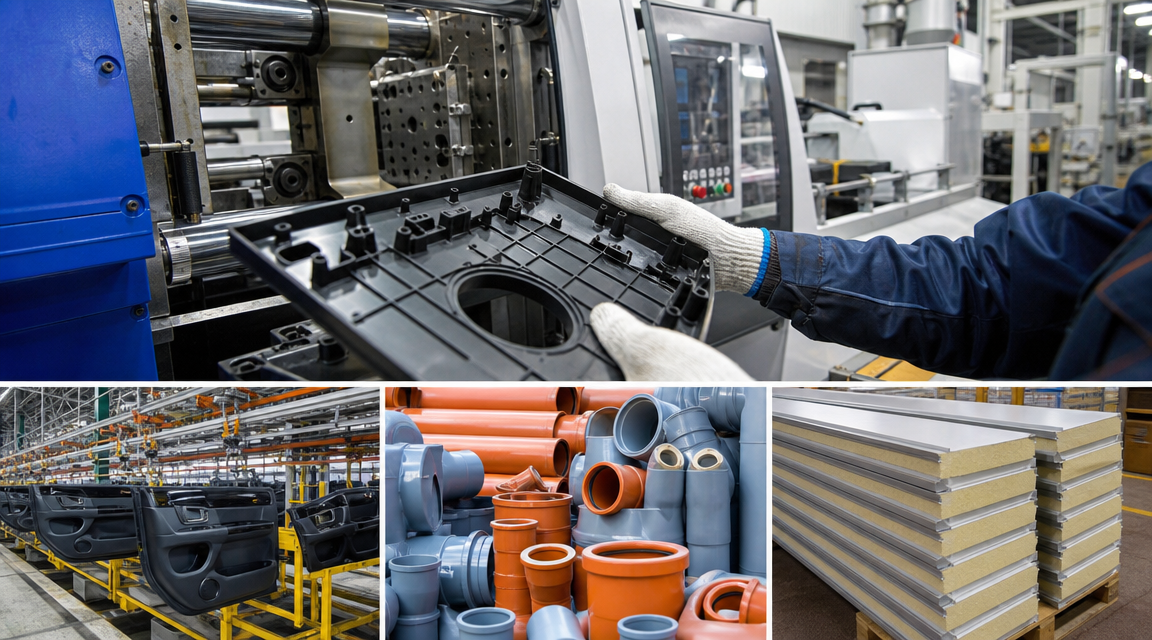

The plastic filler market's expansion is primarily fueled by the burgeoning demand for plastics in packaging, construction, and automotive industries. Fillers are integral to these sectors, offering benefits such as reduced material costs and improved product properties. Their application helps manufacturers achieve specific performance characteristics while managing expenses. This strategic use underscores their economic importance in modern production.

The drive for lightweighting in vehicles and sustainable construction practices is also contributing significantly to market growth. Fillers can enhance the strength-to-weight ratio of plastic components, which is critical for fuel efficiency in automotive design. In construction, they contribute to the durability and longevity of materials, meeting stringent industry standards for longevity. These applications showcase their versatile utility.

The ability of plastic fillers to modify properties like stiffness, impact resistance, and surface finish further contributes to their widespread adoption. These performance enhancements allow plastics to be tailored for diverse applications, from consumer electronics to industrial components. Such versatility ensures a continuous demand across various manufacturing segments globally.

Despite these opportunities, the market faces challenges from volatile raw material prices, which can significantly impact production costs and profit margins for manufacturers. Environmental concerns regarding plastic waste also present a restraint, though some fillers can improve recyclability. These fluctuations necessitate adaptive supply chain strategies and ongoing material innovation.

"The increasing focus on cost-effectiveness and performance enhancement across various industries is a primary driver for the plastic filler market, with demand set to rise significantly over the next decade."

— Market.us Research Team

Segmentation and Regional Outlook

Calcium carbonate continues to dominate the plastic filler market by type, owing to its widespread availability, low cost, and versatile properties. Talc and kaolin also hold significant shares, valued for their ability to enhance mechanical strength and thermal stability. These materials are essential for various plastic formulations, providing key performance benefits across diverse products.

Polypropylene (PP) and polyethylene (PE) represent the largest polymer segments utilizing plastic fillers, reflecting their extensive use in packaging and consumer goods. The demand for filled PVC in construction applications also remains robust, driven by its durability and cost-effectiveness. These polymer types benefit significantly from filler integration, which optimizes their processing and end-use characteristics for specific industrial needs.

Geographically, the Asia Pacific region holds the largest market share, driven by rapid industrialization and high manufacturing output, particularly in China and India. This regional dominance reflects broader global business shifts and economic development patterns. The region's expanding construction and automotive sectors are major consumers of plastic fillers, supporting substantial market volume and continued investment.

North America and Europe also present substantial markets, with steady demand from their mature industries and a focus on advanced materials. These regions are increasingly adopting specialized filler technologies to meet stringent regulatory requirements and consumer preferences for high-performance products. South America and the Middle East & Africa regions are projected for steady growth, driven by infrastructure development and expanding manufacturing bases.

The plastic filler market is on a steady growth trajectory, propelled by consistent industrial demand and evolving material science. While challenges like raw material price volatility and environmental concerns persist, opportunities in bio-based fillers and lightweighting solutions offer new avenues for expansion. The industry's future will likely be shaped by ongoing efforts to balance cost efficiency with enhanced performance and environmental considerations, ensuring fillers remain a critical component in plastic manufacturing worldwide. Strategic investments in research and development will be essential for sustained market leadership and innovation.