At a Glance

- Global market expansion driven by rising vehicle production and safety mandates.

- Technological shift toward 3D imaging systems replaces older manual tools.

- Asia-Pacific region expected to lead global demand for alignment services.

The global automotive wheel alignment system market is entering a period of significant expansion, with growth projections extending through the 2026 to 2035 forecast window. This upward trend is primarily fueled by a steady increase in vehicle production and heightening international safety standards for passenger and commercial transport. Manufacturers are prioritizing precision calibration tools to enhance vehicle handling and reduce tire degradation. As fleet operators seek to minimize maintenance costs, the demand for sophisticated diagnostic equipment continues to rise across both developed and emerging economies.

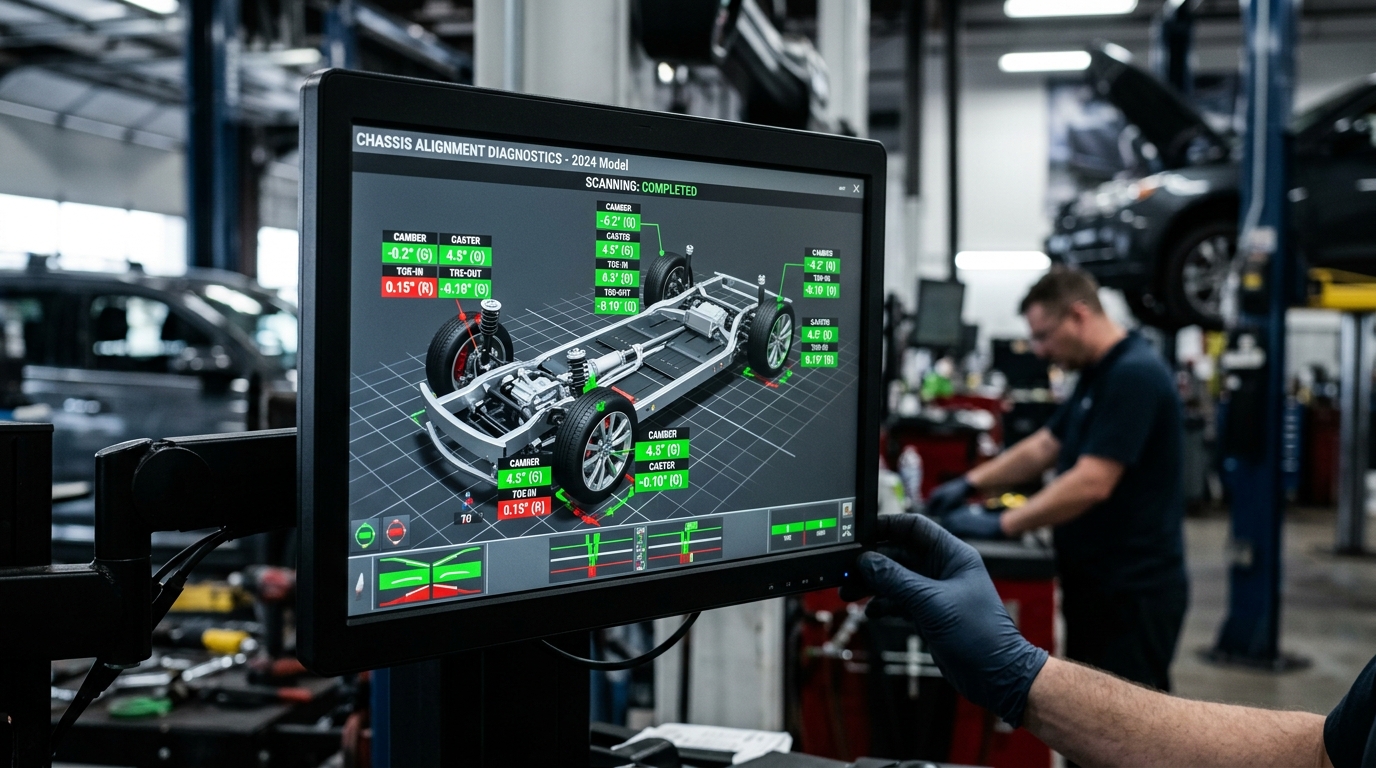

Technological Advancements in Precision Alignment

The industry is witnessing a rapid transition from traditional mechanical systems to advanced digital imaging technologies. Modern 3D wheel alignment systems utilize high-definition cameras and sophisticated software to measure wheel orientation with extreme accuracy. These systems allow technicians to complete adjustments in a fraction of the time required by older CCD sensor methods. By reducing labor hours, service centers can increase their daily throughput and improve overall profitability.

Software integration plays a vital role in the current market evolution as vehicles become more complex. Many new alignment platforms now feature cloud-based databases that store specifications for thousands of different car models. This ensures that mechanics have immediate access to the correct camber, caster, and toe settings for the latest electric and hybrid vehicles. Research Nester indicates that this digital integration is a primary factor influencing purchasing decisions for modern repair shops.

The rise of Advanced Driver Assistance Systems (ADAS) has further complicated the alignment process. Proper wheel geometry is now necessary for the correct functioning of lane-keep assist and collision avoidance sensors. If a vehicle is misaligned, these safety features may fail to operate correctly or provide false readings to the driver. Consequently, alignment checks are becoming a standard part of routine safety inspections rather than just a corrective measure for tire wear.

"As vehicle architectures become more complex, the need for precision in wheel geometry has moved from a maintenance luxury to a safety necessity."

— Alex Richardson, Senior Analyst at Research Nester

Regional Demand and Economic Drivers

Asia-Pacific is positioned as the fastest-growing regional market for wheel alignment technology due to rapid urbanization and rising disposable incomes. Countries such as China and India are seeing a surge in private vehicle ownership, which creates a massive secondary market for maintenance services. Local governments in these regions are also introducing stricter vehicle roadworthiness tests to improve traffic safety. These regulatory changes are forcing smaller independent garages to invest in certified alignment machinery.

In North America and Europe, the market is characterized by a high concentration of premium and luxury vehicles. These automobiles often feature multi-link suspension systems that require specialized alignment procedures and high-end equipment. The growing popularity of electric vehicles in these regions also presents unique technical requirements for service providers. Because EVs carry heavy battery packs, their suspension components experience different stress patterns than internal combustion engines.

The aftermarket segment remains the largest contributor to total market revenue as older vehicles require frequent adjustments. Potholes and poor road conditions in many urban areas continue to drive the need for regular wheel servicing. Additionally, consumers are becoming more aware of the link between proper alignment and fuel efficiency. Small deviations in wheel angles can significantly increase rolling resistance, leading to higher fuel consumption and carbon emissions.

The next decade will likely see further consolidation among equipment manufacturers as they compete for market share in emerging territories. Future developments may include fully automated alignment bays that utilize robotics to adjust suspension components without human intervention. As autonomous driving technology matures, the precision of wheel geometry will become even more vital for maintaining sensor calibration. Industry stakeholders must adapt to these shifting technical requirements to remain competitive in a changing automotive environment.