At a Glance

- Global market valuation expected to rise from $3.6 billion to $5.5 billion

- Compound annual growth rate projected at 3.9% through the next decade

- Asia-Pacific region maintains dominance in semiconductor manufacturing hardware

The global metal etcher market is poised for steady expansion, with new projections indicating a valuation of $5.5 billion by 2035. This growth represents a consistent compound annual growth rate of 3.9% starting from a 2024 baseline of $3.6 billion. The surge is primarily attributed to the escalating demand for modern semiconductor components across the consumer electronics and automotive sectors. As manufacturers prioritize the extreme miniaturization of circuits, the adoption of sophisticated etching technologies continues to accelerate in every major industrial region.

Semiconductor Demand Drives Industrial Growth

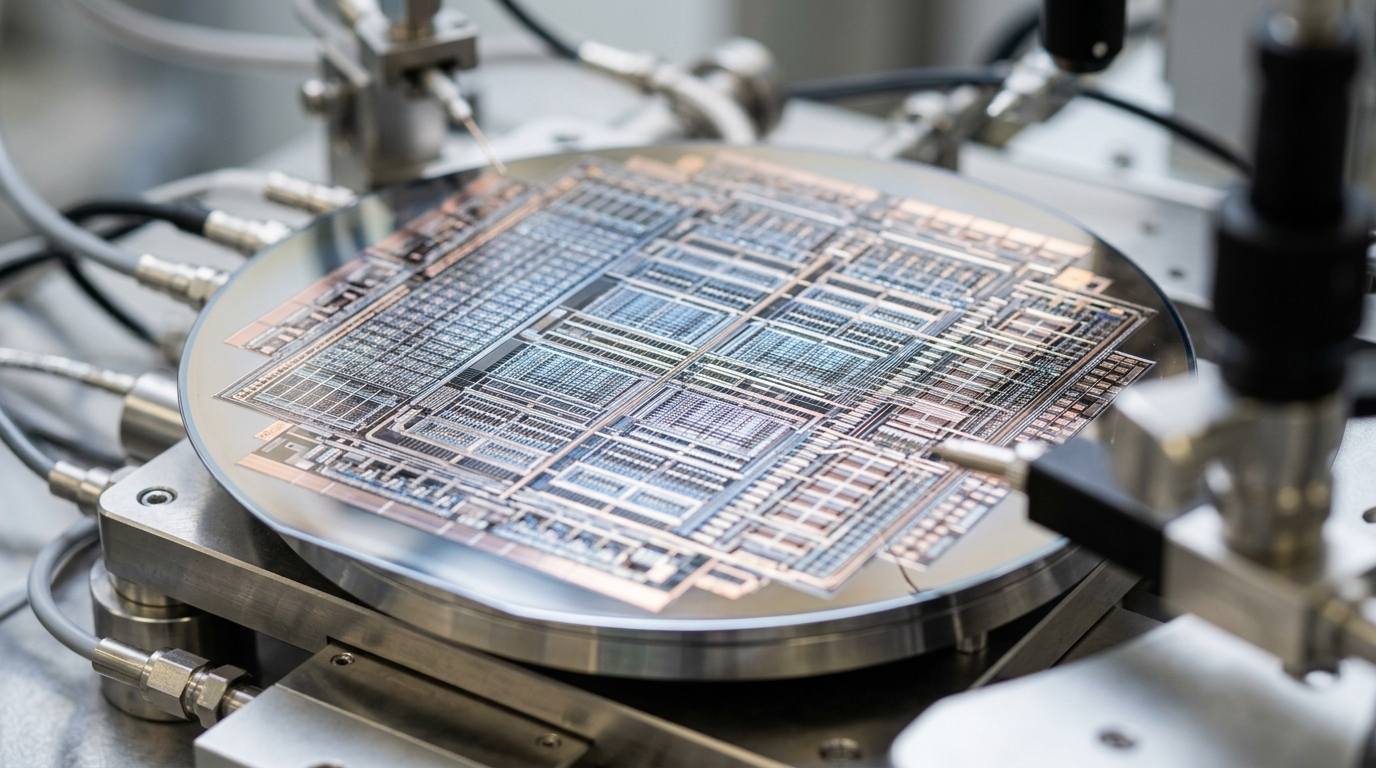

The semiconductor industry remains the primary engine for the metal etcher market as global chip shortages transition into capacity expansions. Increasing integration of electronic systems in modern vehicles requires precise manufacturing techniques to ensure safety and performance. This trend is particularly evident in the production of electric vehicles and autonomous driving systems that rely on high-power semiconductors.

Consumer electronics also contribute significantly to the sustained demand for metal etching equipment. Smartphones and wearable devices require high-density circuit boards that only advanced plasma etching can provide. Manufacturers are currently investing in new facilities to meet the infrastructure needs of the global 5G rollout and future communication standards.

The shift toward dry etching processes is becoming more pronounced as industry requirements for precision increase. Dry etching offers better control over the etching profile and reduces chemical waste compared to traditional wet methods. This transition helps companies achieve higher yields in the production of complex microprocessors and memory units. The data provided by WiseGuy Reports indicates that these technical applications will sustain long-term market stability.

Development of Micro-Electro-Mechanical Systems (MEMS) provides another significant avenue for market expansion. These miniature devices are essential for sensors used in medical equipment, industrial automation, and smart home technology. The ability to etch metals at the micron level allows for the creation of highly sensitive components that are vital for the next generation of internet-of-things devices.

"The expansion of the metal etcher market is intrinsically linked to the global push for smaller, faster, and more efficient electronic devices. As we move toward 2035, the integration of 5G and artificial intelligence will necessitate even more specialized etching solutions to handle advanced chip architectures."

— Senior Research Analyst, WiseGuy Reports

Regional Market Dominance and Competition

Asia-Pacific currently holds the largest share of the global market due to its established semiconductor manufacturing hub. Countries like Taiwan, South Korea, and China are home to major foundries that utilize metal etching at a massive scale. Government subsidies in these regions further support the expansion of local production capacities to secure supply chains.

North America and Europe are also seeing increased activity as they attempt to bring chip manufacturing back to domestic soil. Legislative efforts like the CHIPS Act are encouraging companies to build new fabrication plants in these territories to reduce reliance on overseas shipping. This shift creates a localized demand for etching hardware, installation services, and long-term maintenance contracts.

Key industry participants including Lam Research and Tokyo Electron are focusing on research and development to maintain their market positions. These firms are developing equipment that can handle new materials like gallium nitride and silicon carbide. Such materials are vital for high-power applications in renewable energy systems and aerospace engineering projects.

The competitive environment is characterized by frequent mergers and acquisitions aimed at expanding product portfolios. Smaller firms specializing in niche etching applications are often targeted by larger corporations to fill gaps in their technology stacks. This consolidation helps the major players offer end-to-end solutions for various semiconductor fabrication stages, from initial design to final testing.

Looking ahead, the metal etcher market is set for a period of consistent development as technology requirements evolve. The move toward 2-nanometer and 3-nanometer chip production will require significant upgrades to existing hardware across the globe. While economic fluctuations may present short-term challenges, the fundamental need for advanced electronics ensures a positive long-term trajectory. Stakeholders can expect the market to reach its $5.5 billion target as digital transformation continues to gain momentum across all industrial sectors.